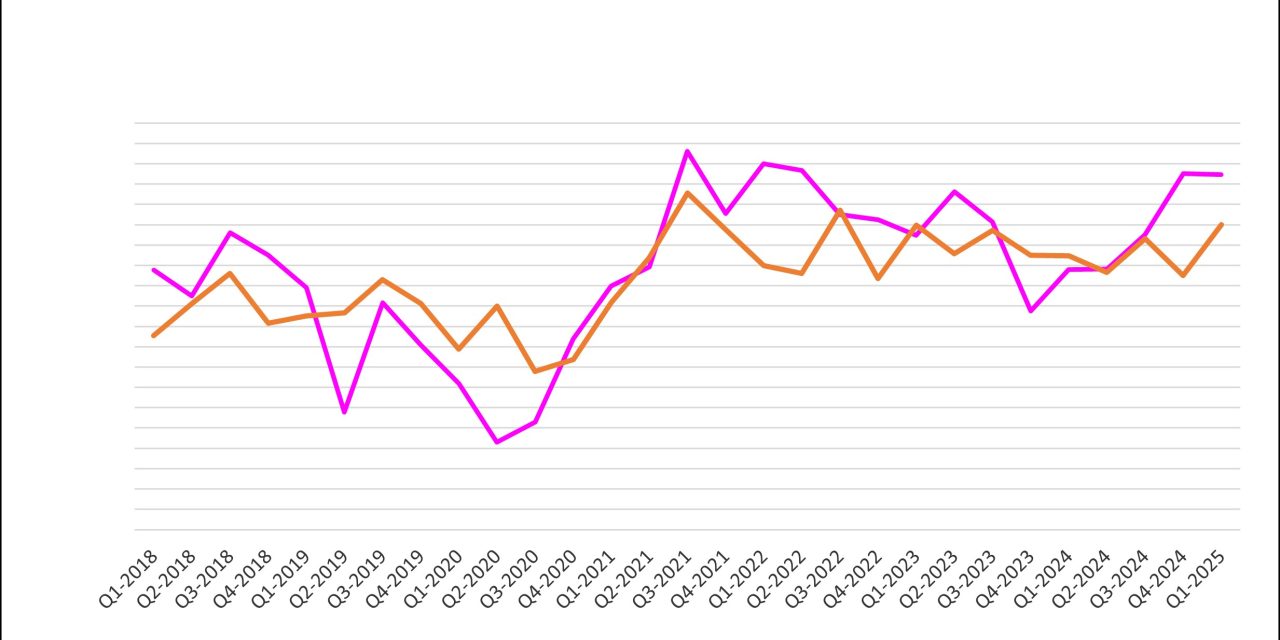

Strong Performance with Sales up 11% up over Q4 2024 and up 7% on Q1 2024.

Strong Performance with Sales up 11% up over Q4 2024 and up 7% on Q1 2024.

Book-to-Bill stays positive at 1.10

Distribution strengthened significantly with an increase of 21%.

Headline results: –

Order intake in Q1 of 2025 was the second highest since Q2 of 2022.

There were some significant variations in market performance.

- Mass Transport up 71% (linked to key rolling stock & infrastructure projects)

- Data Processing saw a jump of 52% (on key datacentre projects).

- Mil/Aero up 24% (a significant increase over 2024 and was the highest revenue level since the end of 2023)

- Medical up 9%

- Communication down 9%

- Test & Measurement down 14% (now falling for two consecutive quarters)

- Broadcast down 16% (against a backdrop of significant spend in 2024).

So, we could be forgiven for thinking that everything was rosy. However, things have since been shaken by the significant tariffs being imposed by the US on the rest of the world, which is definitely not reflected in the data yet.

However, we have seen a significant increase in defence spending, reflecting both the continuing war in Ukraine and probably some pre-emptive spending anticipating that Europe is going to have to fend for itself more.

The second quarter will likely be a far more accurate picture of business levels for the near future and members are naturally extremely cautious.

Nevertheless, the level of RFP’s etc carried into 2025 has helped in holding up Q1 and with a current positive Book-to-Bill there are some faint signs of hope.

Download a full copy of the ITSA Report

ITSA Membership

Is your company active in the UK interconnect supply-chain, but not yet an ITSA member?

If so, why not contact us to find out more about the excellent benefits?

For further information: https://itsa.org.uk/

https://itsa.org.uk/wp-content/uploads/2025/04/ITSA-Q1-Report-2025-v1.pdf